This article serves as an informative overview of the Taxpayer Identification Number (TIN) in the Philippines, highlighting its pivotal role as a unique numerical identifier for registered taxpayers. Essential for transactions with the Bureau of Internal Revenue (BIR), the TIN holds particular importance for new entrants in the workforce.

It focuses on guiding individuals through the process of obtaining a TIN number, detailing the latest requirements, application steps, and associated fees. Notably, it is essential to clarify that while the article offers valuable insights, it is meant as general information and not a replacement for professional advice, emphasizing the significance of seeking expert guidance when necessary.

What is a Tax Identification Number or TIN?

The Taxpayer Identification Number (TIN) is a distinctive and unchanging identifier provided by the Bureau of Internal Revenue (BIR) to individuals. Its primary purpose is to serve as a lifelong identifier, ensuring that each person possesses only one TIN throughout their lifetime.

Regardless of changes in employment status—whether shifting jobs or transitioning from employment to self-employment—it is crucial for individuals to maintain the same TIN. This unchanging nature of the TIN underscores its significance as a constant and unique identifier across various aspects of an individual’s financial and tax-related activities.

How is a TIN Utilized?

The Taxpayer Identification Number (TIN) plays a pivotal role in facilitating the Bureau of Internal Revenue (BIR) with efficient access to and monitoring of taxpayer data and transactions. It operates as a fundamental tool analogous to a bank account number, enabling precise identification of individuals for tax-related purposes.

Much like a bank account number ensures accurate routing of financial transactions, the TIN allows the BIR to effectively record and process tax returns submitted by taxpayers, ensuring the accurate tracking and management of essential financial information.

In What Format and Structure is the TIN Designed?

TIN Length and Components

The Taxpayer Identification Number (TIN) is structured with a variation in length, comprising nine to twelve digits. The primary identification number is constituted by the initial nine digits, holding significance in the identification of the taxpayer.

However, for corporate entities, the last three digits represent the branch code. This distinction is critical in segregating and identifying different branches or divisions of a corporation, enhancing precision in tax tracking and management.

Segmentation and Meaning of Digits

Each digit in the TIN has a specific connotation. The initial digit, ranging from 1 to 9, designates the type of taxpayer, signifying whether the TIN belongs to an individual or a corporation. Notably, 0 is assigned for corporate entities.

For individual taxpayers, the default value for the last three digits is 000. This meticulous segmentation provides a clear understanding of the taxpayer type and allows for effective categorization within the tax system.

Indication of Issuance Period

The issuance period of the TIN is denoted through the first three digits. The 000 series, designated for corporations, and the 900 series, reserved for individuals, were issued before the implementation of the Integrated Tax System (ITS) in 1998. TINs starting with the 200 and 400 series were issued under the ITS, distinguishing them from those issued pre-ITS.

Additionally, TINs commencing with the 300 series are allocated to taxpayers who register online, indicating the different periods and methods of TIN issuance. This diverse series of numbers reflects the historical evolution and differentiates between the various issuance periods, offering insights into the TIN’s origin and issuance methods.

Who is Eligible to Obtain a TIN?

Every Filipino and foreign citizen mandated to fulfill tax obligations in the Philippines must initially register with the Bureau of Internal Revenue (BIR) to acquire a TIN. However, before proceeding with the TIN application, it’s crucial to accurately determine the specific type of taxpayer applicable to your status.

Taxpayers fall into two primary categories: individual and non-individual/corporate. Within each classification, there are specific types of taxpayers. Below outlines the distinct types of taxpayers within these classifications.

Individual Taxpayers

1. Local Employees

Local employees, as designated in BIR tax forms under the classification of “Individuals Earning Purely Compensation Income,” refer to Filipino individuals who derive their income exclusively from salaries paid by employers within the Philippines. This category specifically encompasses a broad spectrum of individuals, including fresh graduates who must secure a TIN as a mandatory pre-employment requirement.

Local employees play a vital role in the workforce, representing those reliant on regular salaries from Philippine-based employers and those embarking on their professional journey, for whom a TIN serves as an initial step in their employment endeavors.

2. Self-Employed

Self-employed individuals, as defined by the BIR, constitute those engaged in a trade, business, or practicing a profession, earning independently rather than through traditional employment. This diverse group encompasses several categories, including:

- Single Proprietors: Entrepreneurs operating businesses registered as sole proprietorships with the DTI.

- Professionals: Individuals earning from their practiced professions, comprising freelancers, lawyers, and those holding PRC licenses like doctors, dentists, engineers, and CPAs.

- Artists, Entertainers, Athletes: Individuals generating income from artistic or athletic pursuits, including actors, singers, dancers, directors, writers, and coaches.

Self-employed individuals form a multifaceted segment of earners, encompassing entrepreneurs, professionals, and those engaged in artistic or athletic activities, all earning independently in lieu of traditional employment structures.

3. Mixed-Income Earners

Mixed-income earners comprise individuals who generate income from multiple sources, encompassing businesses, professions, or employment concurrently. As per the BIR classification, these earners are defined as individuals involved in any combination of local employment, single proprietorship, and professional engagements.

For instance, a mixed-income individual might work full-time for an employer while simultaneously managing a secondary source of income.

When it comes to registration requirements, the BIR mandates these earners to register under multiple categories simultaneously, such as local employees, professionals, and single proprietors if their income stems from these different sources. This classification ensures proper categorization and compliance within the tax system for individuals navigating diverse income streams.

4. Foreigners

Foreign nationals intending to work or establish businesses in the Philippines are required to adhere to specific regulations outlined by the Bureau of Internal Revenue (BIR). To comply with these regulations, they must undergo the following processes:

- Registration with the BIR: Foreign nationals must register with the BIR, initiating their compliance with Philippine tax laws.

- Acquire a Taxpayer Identification Number (TIN): Obtaining a TIN is a crucial step for foreign individuals, enabling them to engage in various financial and tax-related transactions within the country.

- Fulfill Tax Payment and Filing Obligations: It is imperative for foreigners to meet their tax payment and filing obligations in accordance with Philippine tax laws.

In the Philippines, foreigners are categorized as either resident or nonresident aliens based on their residency status. These categories are defined as follows:

- Resident Aliens: Non-Filipino citizens with permanent residency status in the Philippines.

- Nonresident Aliens: Non-Filipino citizens who do not hold Philippine residency but have stayed in the country for over 180 days within any calendar year. This category encompasses expatriates, foreign entrepreneurs, and others among its scope.

Foreigners within the Philippines must fulfill their tax-related obligations based on their categorization as resident or nonresident aliens, complying with the tax laws set forth by the BIR.

5. One-Time Taxpayers

Individuals involved in specific one-time transactions and lacking a previously issued Taxpayer Identification Number (TIN) are required to obtain a TIN and register as one-time taxpayers to fulfill certain tax obligations. These tax requirements include:

- Capital Gains Tax: Levied on individuals profiting from the sale of real properties or shares of stocks.

- Donor’s Tax: Applicable to individuals giving gifts or donations exceeding Php 250,000.

- Estate Tax: Imposed on legal heirs or beneficiaries of a deceased person’s estate.

- Final Tax on Winnings: Applicable to winners of lotto, sweepstakes, or prizes exceeding Php 10,000.

- Motor Vehicle User’s Charge: Mandatory for individuals registering their vehicles with the Land Transportation Office (LTO).

Individuals engaged in these one-time transactions, whether involving property sales, significant donations, inheritance matters, substantial prize winnings, or vehicle registrations, are obliged to acquire a TIN and register as one-time taxpayers to meet their specific tax obligations as required by the BIR.

6. Non-Taxpayers or People Registering Under EO 98

Despite being exempt from income tax, specific groups such as minors, students, housewives, retirees, unemployed individuals, and Overseas Filipino Workers (OFWs) are mandated to obtain a Taxpayer Identification Number (TIN).

This requirement, stipulated by Executive Order (EO) 98, encompasses the directive for all government agencies and local government units (LGUs) to incorporate the TIN in official documents, including forms, licenses, permits, and clearances.

The TIN holds functional significance by enabling non-taxpaying individuals in the Philippines to engage in transactions with various entities such as government offices (e.g., NBI, LTO), as well as financial institutions like banks and stock brokerage firms, facilitating smoother interactions and compliance with EO 98 regulations.

7. Estates and Trusts

The Bureau of Internal Revenue (BIR) imposes the necessity of a separate Taxpayer Identification Number (TIN) specifically for estate tax payments, distinct from the TIN associated with the deceased person or the trustee. Estates are defined by the legal concept encompassing an individual’s net worth, comprising assets like real properties, cash, investments, and insurance.

These assets are subject to taxation upon the owner’s death before being transferred to legal heirs. Conversely, trusts are legal arrangements where a trustor entrusts assets to a trustee for the benefit of a third party, such as a designated beneficiary. In both cases, the BIR requires a distinct TIN for estate tax purposes, maintaining differentiation from the TINs associated with the deceased person or trustee.

Corporate Taxpayers

In compliance with BIR regulations, various entities are obligated to obtain a business Taxpayer Identification Number (TIN) and register as corporate taxpayers. These categories include:

- Domestic Corporations: These are Philippine-based corporations subjected to taxation on income derived from both local and international sources, ensuring taxation compliance within the country.

- Foreign Corporations: Both resident and non-resident foreign corporations fall into this category, being taxed solely on income sourced within the Philippines, irrespective of their operational presence within the country.

- Partnerships: Entities formed by two or more individuals joining hands for a business venture, requiring registration as corporate taxpayers to fulfill tax obligations.

- Cooperatives: These organizations, typically formed to assist members economically, are mandated to acquire a TIN and register as corporate taxpayers to adhere to tax laws.

- Non-stock, Non-profit Organizations: Entities operating for social welfare or charitable purposes, requiring a TIN and registration as corporate taxpayers to comply with tax regulations.

- Associations: This category encompasses taxable or non-taxable entities such as homeowners associations and labor unions, necessitating a business TIN and registration to meet tax obligations.

- National Government Agencies, Government-Owned and Controlled Corporations (GOCCs), and Local Government Units (LGUs): These entities operating at various administrative levels, be it national, local, or government-controlled, are required to obtain a TIN and register as corporate taxpayers in line with tax laws and regulations.

Comprising a broad spectrum of entities from corporations to cooperatives and government agencies, these varied categories are mandated by the BIR to obtain a business TIN and register as corporate taxpayers, ensuring adherence to specific tax obligations based on their respective structures and income sources.

What’s the Significance of Obtaining a TIN?

Acquiring a Taxpayer Identification Number (TIN) is pivotal for multiple reasons and serves as a fundamental necessity in various interactions and transactions within the Philippines. Here are significant reasons why obtaining a TIN is crucial:

Essential for BIR Transactions: A TIN is a prerequisite for tax-related obligations, including filing and payment requirements with the Bureau of Internal Revenue (BIR). It forms the bedrock of compliance with tax regulations, enabling individuals and entities to fulfill their tax responsibilities effectively.

Widely Required as Proof of Taxpayer Status: The TIN is not only pivotal for BIR dealings but is also extensively sought as proof of taxpayer status in various interactions with government bodies, financial institutions, and private companies. It is a mandatory requirement in multiple scenarios, including:

- a. Bank Transactions: Necessary when opening savings, checking, or any form of bank accounts.

- b. Credit and Loan Applications: Vital when applying for credit cards or loans.

- c. Voter Registration: Essential for registration as a voter with the Commission on Elections (Comelec).

- d. Pre-Employment Requirements: Mandatory for new employees to fulfill pre-employment necessities.

- e. Vehicle-Related Transactions: Required when registering vehicles with the Land Transportation Office (LTO) and in transactions involving vehicle, land, house, or condo purchases in the Philippines.

- f. Foreign Worker Permits: Essential for foreign individuals planning to work in the Philippines, aiding in obtaining work visas and employment permits.

The TIN serves as a pivotal identifier and an essential document in an array of financial, bureaucratic, and employment-related processes, making it a fundamental requirement for individuals and entities conducting various transactions in the Philippines.

What are the Steps for Getting a TIN Number in the Philippines?

Securing a Taxpayer Identification Number (TIN) in the Philippines involves two primary methods: walk-in registration and online registration. Walk-in registration requires individuals to visit their designated Revenue District Office (RDO) in person. The processing duration typically ranges from approximately 30 minutes to an hour, contingent on the crowd volume at the office.

On the other hand, online registration can be performed through the BIR eRegistration website, offering a notably faster process, often completed in less than 5 minutes. However, online registration is primarily accessible to registered employers securing TINs for their employees.

Process disparities between the two methods exist, with walk-in registration predominantly involving manual completion of BIR tax forms for most taxpayer types, while the online process is swifter but limited in accessibility, primarily catering to registered employers obtaining TINs for their employees.

How Can You Acquire a TIN Using BIR Tax Forms through Walk-in Registration?

The process of obtaining a Taxpayer Identification Number (TIN) in the Philippines through walk-in registration involves utilizing specific BIR tax forms catering to different taxpayer categories. These forms serve as the initial step in acquiring a TIN for various individuals and entities, ensuring compliance with the BIR’s registration requirements.

BIR Form 1901 – Self-Employed and Various Taxpayers

BIR Form 1901 is designated for self-employed individuals, single proprietors, professionals, mixed-income earners, and non-resident aliens engaged in business activities. This form is also utilized for estate and trust registration, providing a means for different taxpayer types to obtain their TIN.

BIR Form 1902 – Local and Alien Employees Earning Compensation

Primarily intended for new Filipino or foreign employees solely earning salaries in the Philippines, BIR Form 1902 is typically handled by employers. Employees are required to fill out this form and submit the necessary documents for the acquisition of their TIN.

BIR Form 1903 – Corporations, Partnerships, Organizations

For corporate entities, partnerships, non-profit groups, cooperatives, associations, government agencies, and Local Government Units (LGUs), BIR Form 1903 is the designated form to secure a TIN. It serves as an essential tool for these entities to comply with the BIR’s registration and taxation requirements.

BIR Form 1904 – One-Time Taxpayers and EO 98 Registrants

Designed for one-time taxpayers requiring a TIN for specific tax obligations, such as donor’s tax, estate tax, among others, BIR Form 1904 is also utilized by individuals under EO 98. This category includes unemployed Filipinos, Overseas Filipino Workers (OFWs), allowing them to transact with government offices, ensuring compliance with EO 98 mandates.

These distinct BIR tax forms cater to varied taxpayer categories, streamlining the process of TIN acquisition through walk-in registration for individuals and entities falling within different tax brackets and legal requirements in the Philippines.

What are the Steps for Obtaining a TIN Using the BIR eReg Website?

At present, the utilization of the BIR’s eReg system to acquire Taxpayer Identification Numbers (TINs) is exclusively accessible to registered employers or corporate taxpayers for issuing TINs to new employees without existing TINs. Previously, the online registration service was accessible to various taxpayer types, including self-employed individuals and applicants under EO 98.

However, this functionality is currently inactive. Consequently, individuals falling outside the employer or corporate taxpayer categories are required to conduct manual registration at their designated Revenue District Office (RDO). While this scenario may change in the future, the current approach involves employers creating an account in the eReg system to facilitate the issuance of TINs for new employees.

1. How Can You Create a BIR eReg Account?

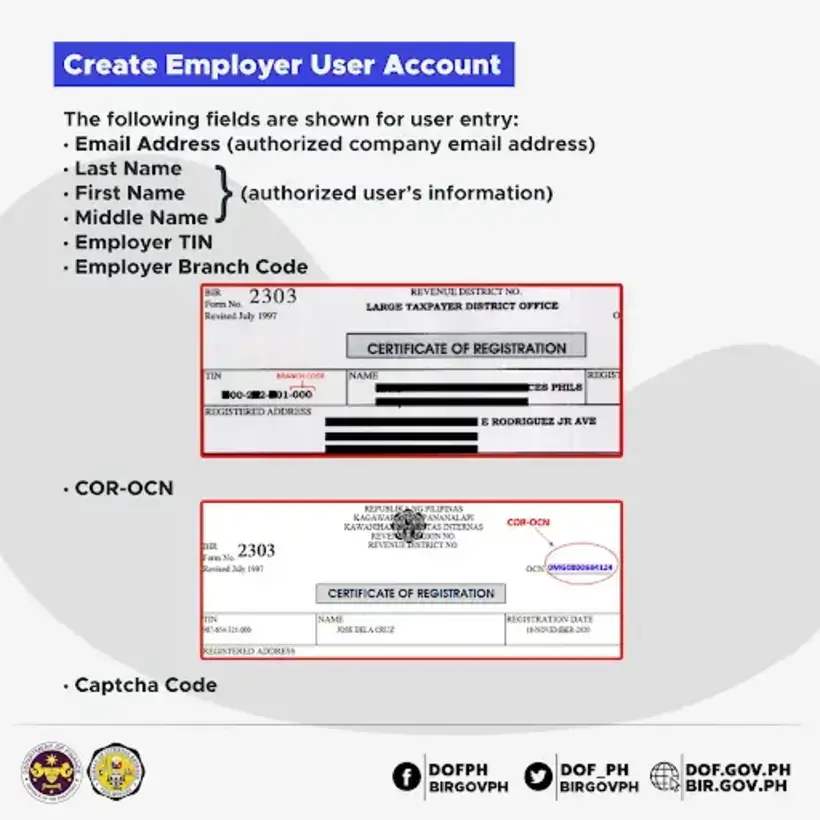

Creating an employer user account on the BIR’s eRegistration website involves a structured set of steps. Here’s a detailed guide:

- Initiate the Account Creation Process:

- Navigate to the BIR eRegistration Website and locate the “Create Employer User Account” option in the User Menu situated on the left-hand side of the page.

- Review the User Agreement, and upon agreement, click the “Agree” button to proceed with the account setup.

- Provide Essential Details:

- Fill in the necessary information, including your email address, complete name, employer TIN, and the employer branch code (comprising the last three digits of your employer TIN, not the RDO code).

- Complete the captcha verification and proceed by clicking the “Submit” button.

- Confirmation and Email Notification:

- After submission, a confirmation message will appear, signaling the successful creation of your account. You will be redirected to the eReg Login page.

- Expect an email notification from the BIR containing your account username, which will be crucial for managing TINs for your employees through the eRegistration system.

Following these outlined steps will facilitate the creation of an employer user account on the BIR’s eRegistration website, granting you the capability to efficiently manage and acquire TINs for your employees using the platform.

2. How Do You Secure TINs for Employees via the BIR eReg System?

The process for employers to issue Taxpayer Identification Numbers (TINs) for their employees through the BIR eRegistration system involves several structured steps:

- Access the BIR eRegistration Website:

- Visit the BIR eRegistration website to initiate the process of issuing TINs for employees.

- Input Username and Email:

- Provide your registered username, which is usually received via email during the account creation process, along with the associated email address.

- Upon matching the details, an email containing your password will be dispatched. Check your spam folder if the email isn’t found in your inbox.

- Complete the Basic Taxpayer Data Form:

- Fill in the requisite information for each employee using the Basic Taxpayer Data Form.

- Required details include the employee’s name, birthdate, name extension, email address, civil status, and gender.

- Note: Taxpayers lacking a middle name must secure their TINs manually at their respective Revenue District Office (RDO).

Upon setting up their BIR eReg accounts, employers can log in to the BIR eRegistration website and furnish necessary employee information via the Basic Taxpayer Data Form to issue TINs for their employees.

How Can You Apply for a TIN if You’re Unemployed?

Acquiring a Tax Identification Number (TIN) is feasible for individuals without current employment status. It’s crucial if an individual doesn’t possess an existing TIN and has a legitimate reason for obtaining one. The application requires the submission of all necessary documentation.

Executive Order (EO) 98 holds significance in this context, enabling students, stay-at-home parents, and unemployed individuals in the Philippines to apply for a TIN. Understanding the specifics of EO 98 is pivotal before commencing the TIN application process at the Bureau of Internal Revenue (BIR).

This executive order provides a means for those not currently employed to obtain a TIN, offering an avenue for various transactions and official engagements as mandated by the BIR.

What Are the Details of Executive Order 98?

Executive Order 98 (EO 98) was introduced by then-President Joseph Estrada, stipulating the compulsory use of Tax Identification Numbers (TIN) in all documents and forms issued during transactions conducted with government agencies and Government-Owned and Controlled Corporations (GOCCs).

The EO made it obligatory for all individuals, regardless of their employment status, to possess a TIN for dealings with both government and private entities. This mandate significantly impacts various transactions and applications, including those for passport, NBI clearance, driver’s license, voter registration, and scholarship applications, necessitating a TIN for each process.

Possessing a TIN holds substantial significance, enabling individuals to obtain valid identification, open bank accounts, apply for scholarships, and engage in a wide array of transactions with different entities, adhering to the mandate set forth by EO 98.

What are the Steps for Getting a TIN Number if You’re Unemployed?

1. Prepare the Required Documents

To initiate the TIN application process, two completed copies of BIR Form 1904 are required. The following documents and considerations are essential for a comprehensive application:

Identification Documents

Identification documents such as the birth certificate, Community Tax Certificate (cedula), passport, driver’s license, or any valid government-issued ID are necessary. These documents should exhibit the applicant’s full name, address, and birthdate.

Married Applicants

For married individuals, presenting a marriage certificate is obligatory during the TIN application process.

Additional Supporting Documents

The BIR may request supplementary documents based on the purpose of TIN registration. For instance, when registering for a TIN linked to bank account opening, a bank certificate specifically labeled “for TIN application only” might be requested.

Bank Certificate Consideration

Some banks might not issue a certification specifically for TIN registration. Prospective applicants aiming to open accounts are advised to check with their respective banks regarding the issuance of a suitable certificate for TIN applications. If unavailable, it might be beneficial to explore other banks offering this particular service for a smoother TIN application process.

2. Download, Print, and Complete BIR Form 1904

For successful completion of BIR Form 1904, essential for Tax Identification Number (TIN) registration for unemployed individuals, follow these instructions:

- Download and Print: Begin by downloading the BIR Form 1904 from the official BIR website and print two copies for completion.

- Filling Guidelines: Adhere to guidelines, using a black ink pen and writing in CAPITAL LETTERS to ensure legibility and accuracy.

- Complete the Form: Provide the required information based on the instructions provided on the form:

- Form Details: Enter the date of TIN application and the specific three-digit code representing the Revenue District Office (RDO) of your city or town.

- Taxpayer Type: Select the appropriate box, marking either “E.O. 98 (Filipino Citizen)” or “Passive Income Earner Only” as applicable to your status.

- Personal Information: Fill in necessary details such as Country of Residence, complete name, local address, birthdate, contact number, mother’s maiden name, father’s name, gender, and email.

- Transaction Details: Choose the purpose for obtaining the TIN. Unemployed Filipinos can select either “Dealings with Banks” or “Dealings with Government Agencies.”

- Declaration: Sign and write your name in the declaration section as a verification of the information provided.

- Additional Form: Ensure that you complete a second copy of BIR Form 1904 with the same diligence and accuracy as the first copy.

By meticulously following these instructions and ensuring the accuracy and legibility of the information provided on BIR Form 1904, unemployed individuals can successfully proceed with their TIN application process.

3. Visit the BIR RDO and present the necessary documents for submission

Start by gathering all the necessary documents required for your TIN application. Ensure that you have your completed BIR Form 1904 and valid identification with you. Upon reaching the Revenue District Office (RDO) in your city or municipality, explain to the BIR officer your intention to apply for a TIN under EO 98. Clearly state the purpose for needing the TIN, ensuring that it is for a legitimate transaction with a government office or bank. Anticipate various scenarios and plan appropriate actions:

- Scenario 1: If you’re informed of ineligibility due to unemployment, politely assert your right under EO 98 for TIN application.

- Scenario 2: If additional documents are requested, having them readily available can expedite the process and prevent the need for multiple visits.

- Scenario 3: In case you are provided with a different form (e.g., 1901 or 1902), clarify your application under EO 98 and use Form 1904 specifically designed for unemployed applicants.

For pre-employment purposes, Form 1902 might be required. Being well-prepared with the correct form and documentation is crucial when applying for your TIN at the BIR RDO. Clearly articulate your application under EO 98 to ensure a smooth process.

4. Await the issuance of your TIN

After you submit the necessary documents at the BIR RDO, the application is processed by the BIR personnel. Upon TIN generation, the BIR will issue a copy of your submitted BIR Form 1904, which will be stamped as “Received” and contain your newly issued Tax Identification Number. Subsequently, the BIR officer at the Revenue District Office will inform you of the date when you can return to claim your physical TIN ID.

Important Tips and Warnings for TIN

1. Single TIN Policy

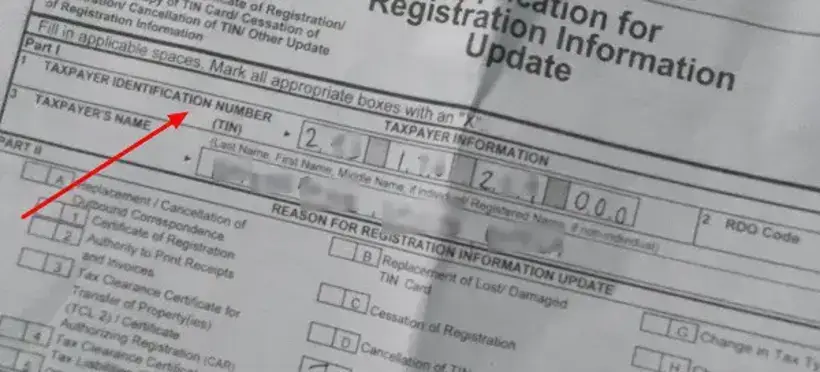

The foremost piece of advice during TIN registration is to avoid obtaining multiple TINs. Even amid changes in employment or business, refrain from securing a new TIN. Instead, consider updating your registration details, especially if moving to a new Regional District Office (RDO).

Furthermore, if you’ve misplaced your TIN, seek assistance for its recovery. Acquiring multiple TINs is deemed an illegal act and is subject to a penalty of PHP 1,000 per additional TIN procured. Therefore, it’s imperative to stick to a single TIN to evade legal complications and financial penalties.

2. Updating Details and Lost TINs

While avoiding multiple TINs is crucial, it’s important to know that updating your TIN details, such as a change in the RDO or recovering a lost TIN, is permitted and crucial. If your details have changed, promptly notify the BIR and update the information to ensure accurate tax filings and compliance.

However, if you’ve lost your TIN, immediately report it to the BIR for assistance in its retrieval. Resolving these issues promptly can avoid complications and penalties in the future.

3. Cancellation of TIN with Business Dissolution

For corporations and partnerships undergoing dissolution or closure, it’s necessary to cancel the associated Tax Identification Number. The termination of a business prompts an investigation by the BIR to evaluate the remaining liabilities of the taxpayer.

Complying with the cancellation procedures for the TIN related to the dissolved business is important to avoid any future legal or financial repercussions and to facilitate the formal closure of the company.

4. Legal Consequences of Multiple TINs

Acquiring multiple TINs might result in legal consequences. Beyond the penalty levied for each additional TIN obtained, it’s also important to note that multiple TINs can complicate tax filings and create discrepancies in records. These discrepancies can lead to issues with the BIR and might result in potential legal action. Thus, adhering to the single TIN policy and ensuring accurate details for the single TIN are crucial.

5. Adherence to Legal Obligations

Ensuring compliance with the BIR and adhering to legal obligations surrounding the TIN is of utmost importance. Whether it’s maintaining a single TIN or promptly addressing changes in details or business status, staying compliant with BIR regulations and laws minimizes legal risks and ensures a smoother tax-filing process.

Taking these precautions and adhering to these legal guidelines provides a safer, more compliant pathway for businesses and individuals.